Come to the Farm Bureau in two weeks to hear

Tax Assessor staff present their updates and provide your input

for changes to the

rural land revaluation, this time taking into account rivers, aquifer recharge zones, and uniformity.

Maybe the Tax Assessors actually don’t want more flooding in Valdosta;

both the City of Valdosta and GA-EDP have already shown interest in attending

about that point.

for changes to the

rural land revaluation, this time taking into account rivers, aquifer recharge zones, and uniformity.

Maybe the Tax Assessors actually don’t want more flooding in Valdosta;

both the City of Valdosta and GA-EDP have already shown interest in attending

about that point.

At an appeal on my property valuation, the Board of Equalization stopped short of actually ordering the Tax Assessors to redo last year’s rural land revaluation, because staff volunteered in the meeting to go ahead and work with the public on ongoing changes, starting with that Farm Bureau meeting. The hearing Board did remark pointedly, while making their ruling of no change to our specific assessment, that we could appeal again next year, or we could even go ahead and appeal to Superior Court this year. Naturally, we’d prefer not to do that, as long as the Tax Assessors move along and do what they promised to do. You are all invited to the upcoming Farm Bureau meeting to help . We’ll post the specifics as soon as we know them. Thanks to Farm Bureau president George Biles for agreeing to set up that meeting.

The Board of Equalization acknowledged we’d made our point that the recent rural land revaluation by the Board of Assessors was not uniform, because of the numerous examples Gretchen Quarterman presented from the book she had prepared. That was before landowner Carolyn Selby, as a witness for appellant John S. Quarterman, spelled out yet more examples of lack of uniformity in last year’s rural land revaluation for both large and small tracts. And before Farm Bureau president George Biles, as another witness, spelled out the point that raising tax valuations on surrounding property leads to land sales that produce subdivisions, resulting in tracts surrounded by subdivisions, which causes those landowners to sell, as well, like just happened with the Webb property. In other words, raising tax valuations drives development to areas so raised. This is what the county and Tax Assessors are doing to this county. If we wanted to live in Atlanta, we would.

Driving development into the agricultural north of the county also adversely affects Valdosta and the south end of the county, by not assisting development close in to existing services, for example on the south side of Valdosta.

The County Commission the previous day had just approved an ongoing contract with GMASS*, Inc. to perform maintenance updates to the Rural Land Schedules for the 2016 Digest. De Gist, who along with Lisa Bryant was representing the Board of Assessors, said in the hearing said that they had already started modifying the Rural Land Accessibility Codes map and underlying data. Board of Equalization hearing Chair Gelana Goddard, with Alternate Joe Clark and Member Lana Hall, said that considering those two points above, that it seemed like the Assessors were going ahead and dealing with the issues of uniformity raised in the hearing, the hearing panel declined to order the Tax Assessors to fix the lack of uniformity, while very pointedly noting our rights of appeal, either next year through the same means, or this year to Superior Court.

*GMASS is Georgia Mass Appraisal Solutions & Services of 3439 Kelly Bridge Rd, Dawsonville, GA, 30534.

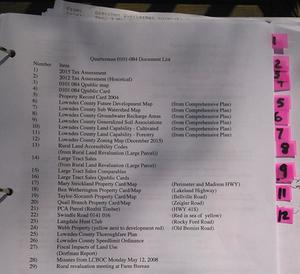

Below is the text of the Quarterman 0101-084 Document List, for the book we gave to each of the three BoE members plus one for the Tax Assessors staff in the hearing. Here I’ve added links to most of the documents that were in the book, plus some narrative notes indicating roughly how the hearing went. The notes are probably not exactly in the same order as events occured, and they are certainly not exhaustive. We planned to have video, but the usual LAKE video camera was at another meeting, and the fallback camera failed; sorry about that. VDT reporter Jason Stewart was also there, and he has a copies of all the documents; his editor may yet agree to him filing a story.

Number Item

1) 2015 Tax Assessment

2) 2012 Tax Assessment (Historical)

3) 0101 084 Qpublic map

4) 0101 084 Qpublic Card

5) Property Record Card 2004The above were all detail on my specific property that I was appealing, which is on Quarterman Road in the far north central part of the county, near the county line.

Then we shifted to the larger context from the Lowndes County Comprehensive Plan, which was agreed on by the entire county as the plan for the future of the county.

6) Lowndes County Future Development Map (from Comprehensive Plan)

7) Lowndes County Sub Watershed Map (from Comprehensive Plan)

8) Lowndes County Groundwater Recharge Areas (from Comprehensive Plan)

9) Lowndes County Generalized Soil Associations (from Comprehensive Plan)

10) Lowndes County Land Capability – Cultivated (from Comprehensive Plan)

11) Lowndes County Land Capability – Forestry (from Comprehensive Plan)

12) Lowndes County Zoning Map (December 2015)Around this point Joe Clark wondered what all this had to do with the specific valuation of our property. We said that wasn’t the main point. As the attendance at the previous Farm Bureau meeting demonstrated, and the presence of the two witnesses we had brought with us, the point was the irregular manner in which the whole rural revaluation was done. Lots of people are thinking not just of their particular property, but of the entire county.

As Chair Gelana Goddard had pointed out at the beginning of the hearing, the Board of Equalization can consider uniformity, not just valuation, per O.C.G.A. 48-5-311.(d)(2), the text of which we had stuck in the back of the book for convenient reference:

If in the course of determining an appeal the county board of equalization finds reason to believe that the property involved in an appeal or the class of property in which is included the property involved in an appeal is not uniformly assessed with other property included in the digest, the board shall request the respective parties to the appeal to present relevant information with respect to that question. If the board determines that uniformity is not present, the board may order the county board of tax assessors to take such action as is necessary to obtain uniformity, except that, when a question of county-wide uniformity is considered by the board, the board may recommend a partial or total county-wide revaluation only upon a determination by a majority of all the members of the board that the clear and convincing weight of the evidence requires such action. The board of equalization may act pursuant to this paragraph whether or not the appellant has raised the issue of uniformity.

Note that last sentence (I added the boldface). It doesn’t even matter whether you checked “uniformity” on your appeal card when you filed. The Board of Equalization can consider uniformity anyway. And if the Board finds lack of uniformity, it has the power to order the Tax Assessors to fix it (the middle sentence I set in larger type).

Quoting the Georgia law was necessary because both Ellis Black and Mike Hill had told us at the previous Farm Bureau meeting that the Board of Equalization could only consider specific parcels, not general and systemic issues. That is simply not true according to the state law that set up the Board of Equalization: in fact they can consider uniformity, and they can even order the Tax Assessors to fix it.

So that left the requirement of the first sentence: presenting relevant information.

13)

Rural Land Accessibility Codes (from Rural Land Revaluation (Large Parcel))

This map from the Tax Assessors’ Rural Land Revaluation (Large Parcel) does not match the maps from the Comprehensive Plan, especially for the northern part of the county, and for the rivers and aquifer recharge zones.

Joe Clark asked what did we mean when we said the whole county had agreed on the Comprehensive Plan. I said there were public meetings for input, some of which I attended back in 2005, after which all the elected bodies in the county held public hearings and voted to approve the Comprehensive Plan, including the County Commission and the City Councils of all five cities: Valdosta, Remerton, Hahira, Dasher, and Lake Park. Gretchen noted there were updates every five years in a similar process, and we’d just attended a public input workshop Monday for the current update. That seemed to satisfy the Board that the Comprehensive Plan really is the plan agreed upon by the whole county.

It’s pretty clear just by looking at it that the Tax Assessors’ Rural Land Accessibility Codes map does not match the Comprehensive Plan maps, nor the current Lowndes County zoning map, and in numerous places blatantly contradicts them.

Gretchen proceeded into detail about last year’s Rural Land Revaluation (Large Parcel). The Board of Equalization member had not seen that document, and the Tax Assessor staff had not brought any copies with them, but we had an extra copy, which we provided to the hearing board, along with the extracts in the book.

14) Large Tract Sales (from Rural Land Revaluation (Large Parcel))

15) Large Tract Sales Comparables

We brought up that in the previous Farm Bureau meeting either Chief Appraiser Silar Hrobar or Tax Assessor Mike Hill had said that accessibility didn’t really mean proximity to roads and road frontage only applied after staff decided on geographical areas of similarity. I had repeated it back to him and he confirmed that it was staff and not the consultant who made such decisions.

De Gist said that actually she had first gotten a draft from the consultant taking into account such criteria and then she had worked with them to modify it. We pointed out that was not what we were told in the Farm Bureau meeting, and we had four witnesses sitting at the table right then in the hearing (Gretchen, jsq, Selby, and Biles), plus video of the Farm Bureau meeting.

De Gist said she was working to represent the concerns of taxpayers. We thanked her for that.

16) Large Tract Sales Qpublic Cards

De Gist said the Rural Land Accessibility Codes areas of geographical valuation had been decided on the basis of prior sales. You can readily see if you follow the links below to the maps of the actual comparable sales listed by the Tax Assessors that none of these sales were in the north Lowndes area where my property is, yet that area is shown in red in a highest valuation geographical area.

We also pointed out numerous other discrepencies, such as the two sales to Bill Gates in and near Lake Park that were used as benchmarks and are next to US 42 South, yet are not shown as hightest valuation.

- 0040 007 6120 Rowland Road,

- 0137 032A 6066 Clyattville-Lake Park Road,

- 0189 191 636 Tince Road, Lake Park, GA 31636,

- 0216 046 4180 Boring Pond Road,

- 0222 002 6734 HWY 376, Lake Park, GA, right between some Bill Gates purchases.

- 0222 004, HWY 376, Lake Park, GA, next to the previous,

- 0224 003, east of Lake Park, next to the previous, and this one is a Bill Gates purchase,

- 0237 001 4707 Humphreys Road, Naylor, another Bill Gates purchase,

- 0237 015 0 Otter Creek Road, Naylor,

- 0261 011 on Wiggins Road and Mullins Lane, Naylor, GA

Next Gretchen presented numerous parcels that are comparable to our tract, but that were not included in the revaluation comparables. Chairman Goddard remarked several times during the hearing that the online Tax Assessors maps available through qpublic were not reliably up to date, and anybody who wanted current information should go down to the Tax Assessor office. I noted that nonetheless the comparables Carolyn Selby had gotten through qpublic for her appeal were not challenged by the Assessors’ staff in any way.

17)

Mary Strickland Property Card/Map (Perimeter and Madison HWY) 0167 121

This is right across from the airport. Why isn’t it in a red region?

18) Ben Wetherington Property Card/Map (Lakeland Highway) 0210 002

19) Taylor-Slocumb Property Card/Map (Bellville Road) 0227 015

20) Quail Branch Property Card/Map (Zeigler Road) 0228 001. This is the location of the County Commission’s recent planning days, and of the annual Lake Park Chamber of Commerce dinner, at which Tax Assessor W.G. Walker presided this year. It’s also between Lake Park-Bellville Road and US 41 South and quite near I-75. Why is it not in a highest valuation area? Sure, it’s currently on a dirt road, but so are numerous other parcels which are in highest valuation areas.

21) PCA Parcel (Rozbit Timber) (HWY 41S) 0228 002, and continuing almost to I-75: why isn’t this in a highest valuation geographical area?

22) Swindle Road 0141 016 (Red in sea of yellow) 0141 016

23) Langdale Hunt Club (Rocky Ford Road) 0037 001

24) Webb Property (yellow next to development red) (Old Bemiss Road) 0145B 094. Why was this property marked as yellow, if sales are really the criterion?

25)

Lowndes County Thoroughfare Plan

This plan, which few people seem to know about, including incoming elected Lowndes County Commissioners until we told them about it, assigns classifications ranging from local rural road to minor collector to major collector upwards through artery. These classifications matter for rezoning. Classification as a collector or higher gives local landowners rights to do things like create a cemetery on their road. When this Thoroughfare Plan was last updated, in 2009, County Engineer Mike Fletcher said in a public County Commission Work Session that it

…works as a guide for development and potential use changes in property.

Tax Assessor staff took roads and their classifications into account in their assignment of geographical regions and of specific property valuations, so clearly they were incorporating by reference the county’s “guide for development and potential use changes in property”.

Remember, as Tax Assessor Mike Hill told us in the previous Farm Bureau meeting:

Paving roads drives development.

Therefore it is our contention that the Tax Assessors are working with the county government to drive development where they want it to go. And clearly by the Codes map that includes straight north from Valdosta all the way to the county line through the rural agricultural and forestry area of north Lowndes, as well as through aquifer recharge zones and to the rivers. This is blatantly inconsistent with the Comprehensive Plan that all the elected governments in the county decided on. And the rural land revaluation that produced that map is clearly not uniformly assessed with other property included in the digest.

26) Lowndes County Speedlimit Ordinance [VDT story]

After reclassifying numerous local rural roads to minor collectors, and some minor collectors to major collectors, the county also paved some of them and raised speed limits. All this drives development. And the Tax Assessors’ plan follows that drive to the north of the county.27) Fiscal Impacts of Land Use (Dorfman Report)

We’ve had this online since 2007: The Local Government Fiscal Impacts of Land Use in Lowndes County: Revenue and Expenditure Streams by Land Use Category, Jeffrey H. Dorfman, Ph.D., Dorfman Consulting, December 2007. As Dr. Dorfman summarized in a different presentation,

Local governments must ensure balanced growth, as

sprawling residential growth is a certain ticket to fiscal ruin*

* Or at least big tax increases.

This is because it costs the county a lot more to service subdivisions the farther out they are from county services, and costs the county school system even more to run school buses. Conversely, trees and crops don’t call the sheriff or the fire department much, so forestry and agriculture are far more cost-effective in tax collection vs. services.

28) Minutes from LCBOC Monday May 12, 2008

Since Lowndes County no longer keeps minutes online farther back than 2008, fortunately LAKE keeps copies, and I’ve put the 12 May 2008 Work Session Minutes online on the LAKE website, and copied the relevant paragraph below:

Local Government Fiscal Impact of Land Use in Lowndes County, County

Manager, Joe Pritchard, requested that the Commission acknowledge the presence of Dr. Jeffrey Dorfman. Further, Dr. Dorfman was in attendance for the purpose of formally presenting the Lowndes County Fiscal Impact Study that was previously distributed to the Commission at their annual planning retreat. Dr. Dorfman addressed the Commission regarding the contents of his report to include data regarding the importance of planning and the impact current growth has on the fiscal viability of Lowndes County. Dr. Dorfman further stated that Lowndes County government was doing an excellent job managing the cost of providing services to residents. Mr. Pritchard added that County Planner, Jason Davenport, and Dr. Dorfman would be meeting with members of the Home Builder’s Association in an effort to answer any of their questions related to the study.

It shows that Dr. Dorfman did present his plan to the Lowndes County Commission. I was at the followup meeting with the Home Builder’s Association, so I can attest to that, too. However, none of those Commissioners are still serving, and none of the new Commissioners were told about this Dorfman report, so far as I could discover by asking them. All this seemed to be new to the Board of Equalization, although perhaps not to the Tax Assessor’s staff, since we did mention the Dorfman report at the previous Farm Bureau meeting.

At the end of our presentation, the Chair asked for the Tax Assessors staff to present. They started by saying there’s no way any of what we asked for would ever happen, because only sales could be taken into account. However, with some discussion it quickly became clear that staff were in fact already taking into account numerous other criteria, including soil types, wetlands, roads and road classifications, etc.

It’s only a small step from wetlands to also use “as tools in their toolbox” rivers and aquifer recharge zones, for example. And they agreed to do that.

They even asked us how we would suggest they proceed. Gretchen suggested another meeting at Farm Bureau, to which they agreed. George Biles had already left at that point, but I called him afterwards and he readily agreed as Farm Bureau president to contact the Assessors’ office and see about organizing such a meeting.

Finally, the Chair closed the discussion part of meeting and went into the decision part. As mentioned, the board declined to make any changes in our evaluation or to order the Tax Assessors to make any changes regarding uniformity. However, the board pointedly noted this was because Tax Assessor staff had already volunteered to get on with it as noted above, and we had opportunities to appeal, either next year or soon to the Superior Court.

According to O.C.G.A. 48-5-311.(g)(2) we have 30 days to file an appeal with Superior Court. O.C.G.A. 48-5-311.(g)(3) says:

The appeal shall constitute a de novo action. The board of tax assessors shall have the burden of proving their opinions of value and the validity of their proposed assessment by a preponderance of evidence.

I am not an attorney, but I believe “de novo” means we can bring in new witnesses, evidence, and arguments.

O.C.G.A. 48-5-311.(g)(4)(A) says such an appeal “shall be heard before a jury”. A jury trial could be quite interesting, considering how many people around the county are very displeased by this revaluation. One hopes the Tax Assessors’ staff will demonstrate at the upcoming Farm Bureau meeting that no such appeal is necessary.

Thanks to the Board of Equalization for listening and being easy to work with. Thanks to the Tax Assessors’ staff for promising to fix the uniformity problem.

-jsq

Short Link: